Condos v. co-ops: These two types of homes may at first seem the same, but condos are easier to buy and sell. That’s one reason NYC developers have built 46,311 condo units in 2,097 buildings in the last ten years, compared to just 656 co-op units in 16 buildings.

When you buy a condo, you own that specific unit and share ownership of common spaces with other owners. By contrast, a co-op owner does not own the unit in which they live. They own shares in the whole building, which is a nonprofit corporation. The corporation gives buyers proprietary leases that give them permanent rights to occupy their unit, even though they do not own it.

Co-ops came to NYC in the nineteenth century and dominated the market for decades. They were especially popular in the Upper West Side, and even today, most NYC buildings are co-ops. Condos became more popular in the 1970s and now dominate new construction, especially in neighborhoods that have recently risen in popularity.

This article explains why buyers today may prefer condos.

Financing for condos v. co-ops

Condos are significantly easier to finance than co-ops. The latter often entail stringent requirements. Co-op boards commonly require down payments of 30%, whereas many condos will accept a down payment of 10%.

What’s more, lenders are often wary of handing out mortgages for co-ops because co-ops maintain stricter rules. For example, co-ops may limit to whom you can sell your shares. Banks do not want to deal with the red tape and, therefore, may not even offer co-op loans.

Board approval for condos v. co-ops

Condo boards are less strict than those of co-ops. Co-ops usually require interviews. They can reject applicants for a perceived negative attitude toward possibly rigid building rules; as a prospective buyer, you’re joining their community. Co-op boards also take a stricter approach to reviewing your finances. In addition to a relatively large down payment, the co-op board will scrutinize your debt-to-income ratio and post-closing liquidity. This means you may need substantially more money in the bank to a buy a co-op that, on its face, costs the same as a condo.

By contrast, condos usually do not require interviews. The down payment and other financial requirements are more lenient. The condo board will set rules for how you use property, but it does not have a veto over to whom you sell your property.

Closing process

Condos come with higher closing costs than co-ops. For one, condos tend to cost more than co-ops, and many closing costs are a percentage of the home price. But in a 1:1 comparison, condo closing costs are higher because they include a mortgage recording tax and usually title insurance.

Co-op buyers don’t need to do this because they’re technically not buying an apartment but rather shares in a nonprofit. Therefore, you get a deed at a condo closing. But you get a proprietary lease for a co-op.

Tax lot

If you sell your co-op or condo for a higher cost than its purchase price, you will have to pay taxes on the increase in your investment. This is a capital gains tax. You calculate it by subtracting the cost basis (your purchase price plus the cost of any capital improvements) from the sales price minus commissions and closing costs.

In other words, capital gains = (sales price – commissions and closing costs) – (your original purchase price + capital improvements). So, if you sell your apartment for $1 million, have $100,000 in commissions and closing costs, your original purchase price was $500,000, and you made $50,000 in capital improvements, you have $350,000 in capital gains ($900,000 – $550,000). The government won’t tax the raw number. Part of it will be excused from taxes.

Ideally, as a seller, you want any changes to your building or unit that increased its price to count as capital improvements. This would increase your cost basis and diminish your taxable capital gains, resulting in lower taxes.

On this point, co-ops offer an advantage. Changes to the overall building that boost your unit’s value constitute capital improvements and will lower your capital gains tax liability. That’s not the case for condos in most cases.

PPSF

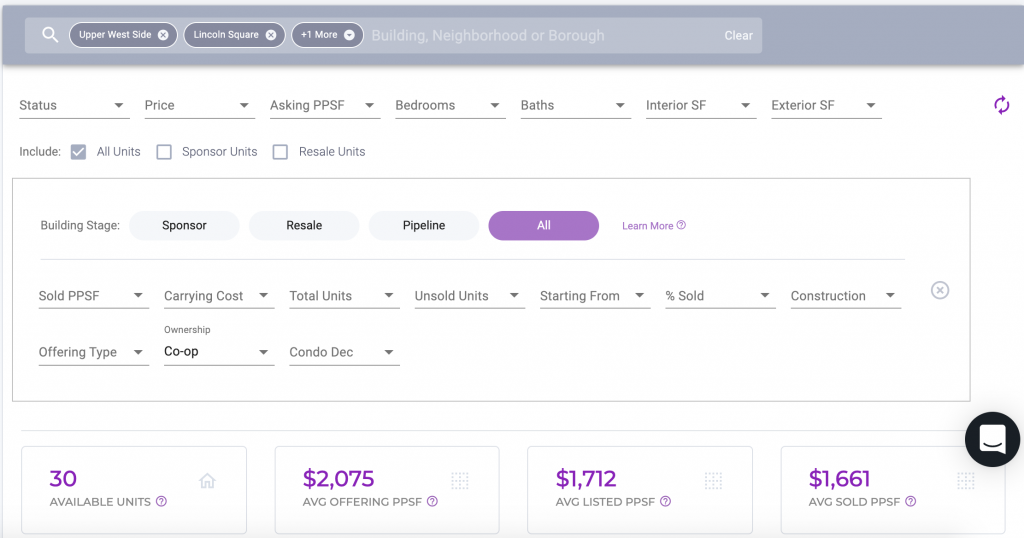

Condos are more expensive than co-ops per square foot. Marketproof Pro data shows that the average PPSF for which Upper West Side co-op units have sold in the last 10 years is $1,661.

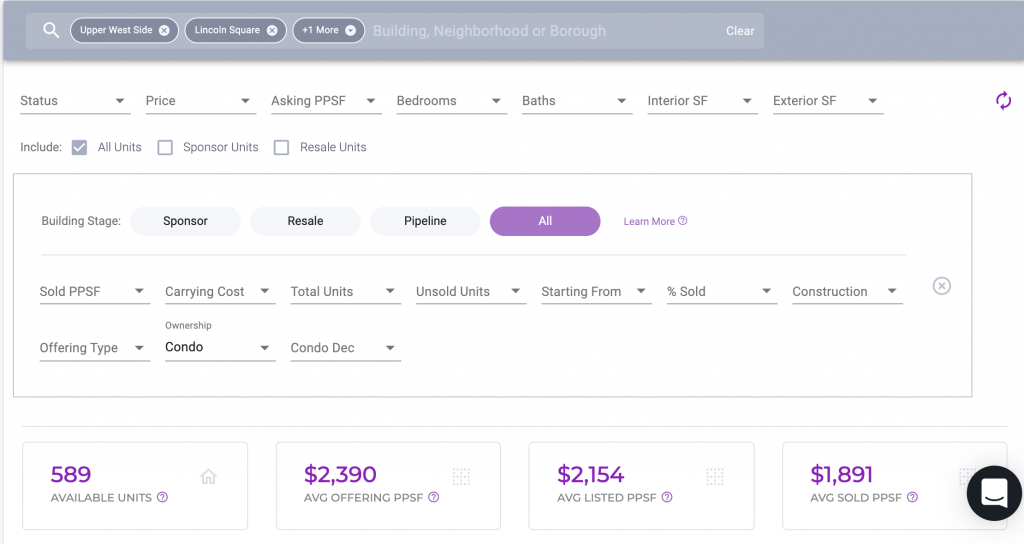

However, the average PPSF for which condo units in the same neighborhood has sold is $1,891.

The price differential between the two types of homes reflects a disparity that generally exists across NYC.

Still, if you can afford the investment, the greater expense of new condos is not necessarily a reason to stay away. These apartments are growing faster in value on average than co-ops, typically making them a stronger investment.

With Marketproof Pro, you get an unparalleled view of NYC condos, empowering you to navigate the market as a real estate professional, investor, or first-time buyer.

Marketproof Pro

Marketproof Pro combines property data, ownership records, market analytics, and AI-powered marketing tools in one place. Search buildings and addresses, look up owners, track sales trends, and create branded reports.