NYC condo and co-op buildings have key documents that mark their progression from construction onwards. This is similar to birth and marriage certificates in the life of a person.

Marketproof mines all of these real estate documents to uncover everything there is to know about NYC condos.

Here’s an overview of the 10 of the most important documents.

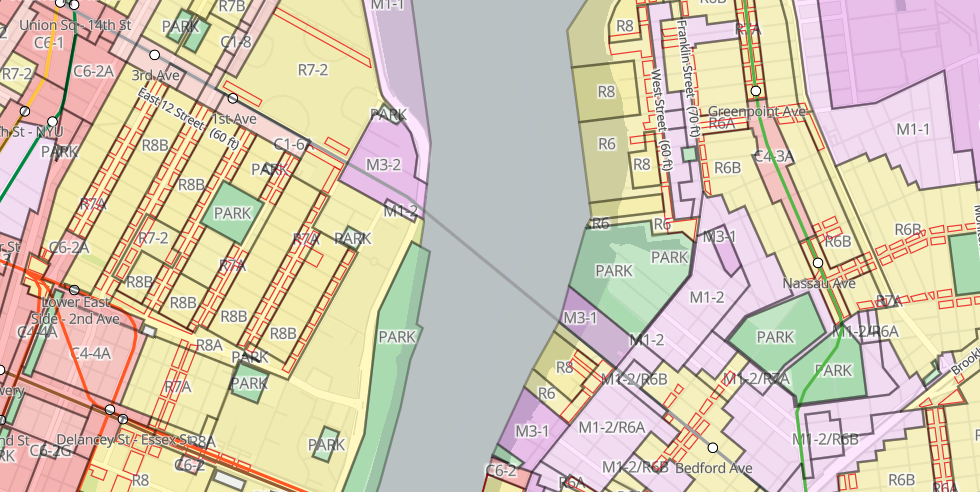

Zoning Map

Before a developer can even consider buying land on which to build residential housing, they will have to see what the land is zoned for. The easiest way to do this is to consult a zoning map.

In New York, there are four main types of zoning: Residential, Commercial, Manufacturing, and Special Purpose. Each type has its own sub-divisions as well.

A developer who is building condos will want to build on residentially zoned land. There are 10 divisions of residential zoning, and the developer will choose which category fits their purpose.

However, just because the land is not residential does not mean that it may not have its zoning changed in the future. A developer can work through the city’s zoning process in an effort to get the zoning of a building changed.

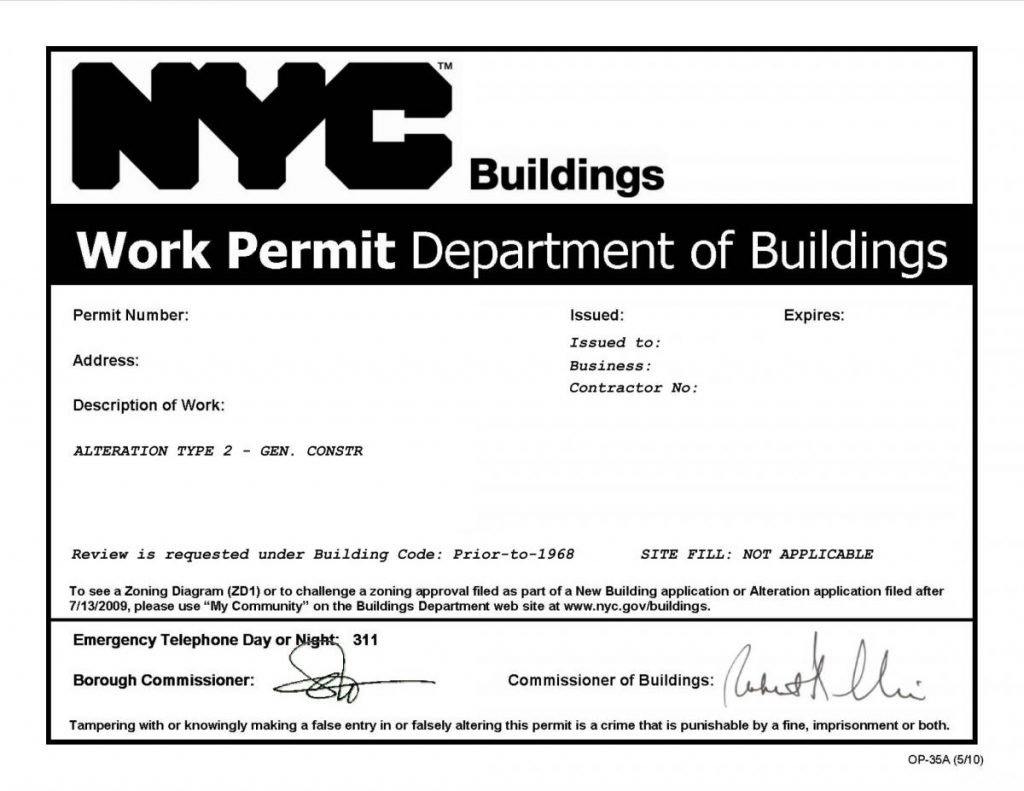

Building Permit

Once the land has been allocated for a new building, the process of obtaining a permit to build on that land starts.

In actuality, the two processes often start at the same time. But the city cannot issue a permit without a secured location.

The permitting process starts with hiring an architect to file plans with the Department of Buildings. There are numerous types of building permits. The architect or engineer will need to file an NB (New Building) permit. New York City laws require that the developer obtain one or more permits before starting construction work. (Refer to NYC Building Code §27-126 for work that requires a permit.)

You can track building permits on Marketproof here:

https://marketproof.com/feed?topic=major-construction

Recorded Sale

When the seller and buyer sign a deed, they ratify the sale of a property, including land. Then, a new title is recorded.

The Office of the City Register records and maintains New York City Real Property and certain Personal Property transfers such as mortgage documents for property in all boroughs except for Staten Island. The Richmond County Clerk records the sale of properties on Staten Island.

Property documents are recorded and maintained on the Automated City Register Information System (ACRIS). ACRIS provides online access to property documents and data dating back to 1966.

You can track recorded sales on Marketproof here:

https://marketproof.com/feed?topic=recently-sold

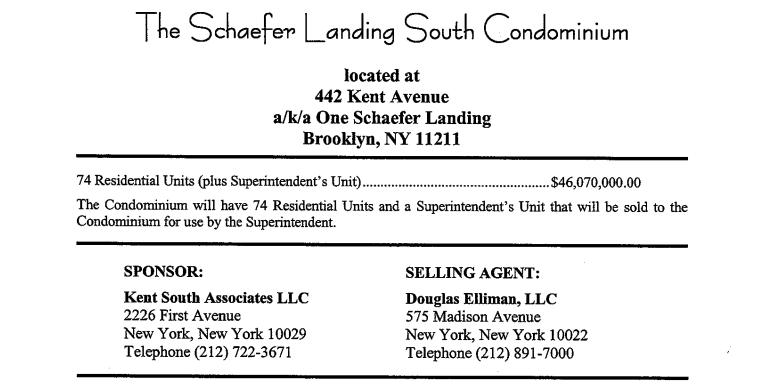

Offering Plan

The offering plan is a disclosure document for prospective buyers that contains vital information about a condo (or co-op). The offering plan’s contents include pricing, buying procedures, floor plans, building bylaws, etc.

The Attorney General’s office requires the document to oversee the structure and use of the building. The AG also ensures the sponsors are selling what their plan shows.

You can track offering plans on Marketproof here:

https://marketproof.com/feed?topic=in-the-pipeline

Condo Declaration

A Condo Declaration is a legal document that lays out what was built, who owns and can use the building, and how it will be operated when control of the condo is transferred from the developer to the condo owners.

The ‘condo dec,’ as professionals call it, operationalizes the plan provided to buyers in an offering plan. The offering plan sets forth what events must take place for this change of control to happen.

The offering plan is a disclosure document that guides the sales process. By contrast, the condo dec is a document that describes the operations of the building over the life of the condo.

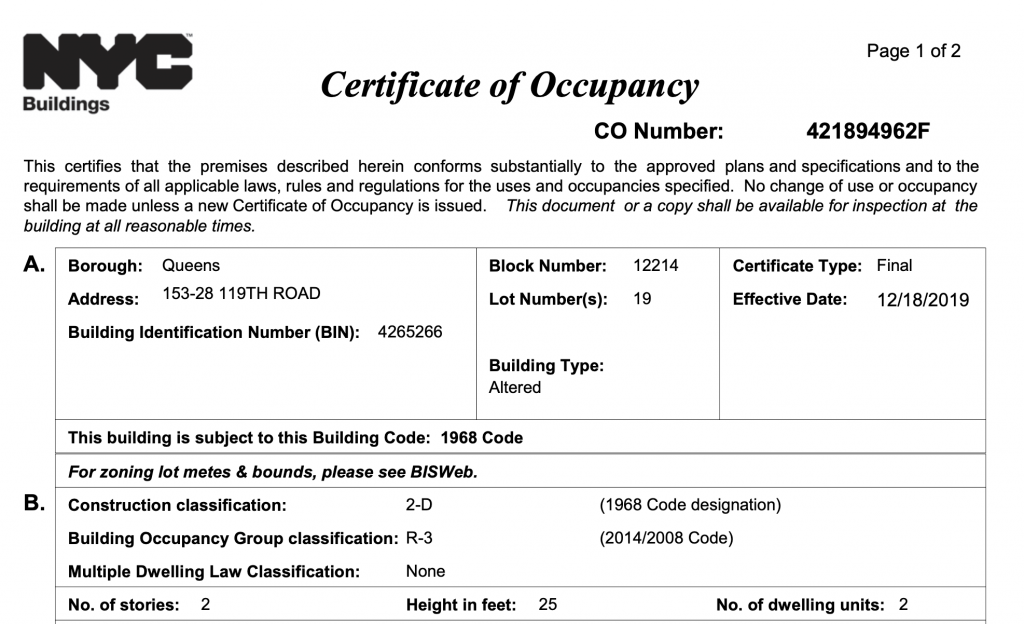

Certificate of Occupancy

A Certificate of Occupancy certifies the legal use and occupancy of a building. The Certificate describes how a building may be occupied. In the case of a condominium building, a Certificate of Occupancy (CO) will describe how many residential units the building contains and how many commercial (if it has those).

A CO is usually necessary when selling a home or refinancing a mortgage. Owners must obtain a new or amended Certificate of Occupancy for new buildings or where construction changes the use, egress, or occupancy to an existing building before the building may be legally occupied.

A CO cannot be issued unless all paperwork is completed, all necessary approvals have been obtained from other appropriate City agencies, all fees owed to the Department are paid, and all relevant violations are resolved.

The CO also includes a property’s BIN and BBL.

You can track certificates of occupancy on Marketproof here:

https://marketproof.com/feed?topic=major-construction&status=temporary-co-issued

Bylaws

The Bylaws in a condo are the rules and regulations that govern the condo owners. They also protect the interest of the owners. They are a self-governing document for the condo association.

The bylaws cover board member qualifications and the direction of the board of directors, including how it administers policies according to the bylaws and how it oversees the maintenance and administration of the association. The bylaws will also cover meetings, voting, proxies, budget, assessments, including special assessments, insurance coverage, and restrictions on the use of the units and the common areas.

They can cover all aspects that the board agrees to be included such as whether the owners can own pets, whether smoking is allowed in the building, and much more.

In a co-op, bylaws differ slightly. They dictate how the corporation operates and dictate to the people living in the co-op what they can and can’t do with respect to living in the building.

House Rules

The term may sound like something posted in a student dorm or youth hostel, but house rules can also apply to multi-million dollar condos and co-ops. Just like in a dorm, the house rules in a condo or co-op refer to the rules governing day-to-day things you can and cannot do or have in a particular co-op or condo building.

They may refer to the hours residents can use certain amenities such as a pool or gym or a laundry room. They will certainly include recycling rules and whether pets are allowed.

House rules may also cover subletting and Airbnb rentals as well as days and hours for move-ins and -outs. They may also include fines for when tenants break rules.

The house rules usually appear in a condo’s main governing document, called the declaration of covenants, conditions and restrictions, or CC&R.

Financial Statements

A condo and co-op’s financial statement is, as the name suggests, a record of the building’s finances. This includes its income and expenses, its cash reserves and assets.

It will show how much the building owes in debt (mortgages) and how much it pays in taxes as well as all maintenance costs.

In larger buildings (20 units and up), there are audited financial statements that are typically prepared by an independent, Certified Public Accountant (CPA) who has followed specific, independent confirmation and diligence procedures to verify that the information they are signing off on is accurate. The CPA will add their notes to the end of a Financial Statement summarizing and clarifying the information provided in the previous sections.

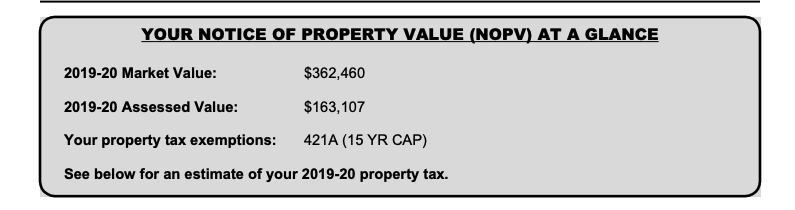

Notice of Property Value

Every January, the Department of Finance mails each property owner in New York City a Notice of Property Value (NOPV). NOPVs gives an owner information about their property, including its assessed value, market value, exemptions, and property description.

It is not a tax bill and does not require payment. The property’s taxes are, however, calculated from its assessed value. In addition, if an owner disagrees with the city’s assessment, they can challenge this value.

You can track Notices of Property Value on Marketproof by going to the Taxes tab on any property. Here is an example:

https://marketproof.com/building/brooklyn/dumbo/100-jay-street-11201/unit-4f?tab=taxes

Marketproof Pro

Marketproof Pro combines property data, ownership records, market analytics, and AI-powered marketing tools in one place. Search buildings and addresses, look up owners, track sales trends, and create branded reports.